What is the EU Taxonomy?

The Taxonomy Regulation (Regulation (EU) 2020/852 of June 18, 2020 on the establishment of a framework to facilitate sustainable investment) is a central component of the EU Action Plan on Sustainable Finance, which introduced a classification system for sustainable economic activities.

With Sustainable Finance, the European Commission is creating a legal framework that places the so-called “ESG” factors at the center of the financial system. In order to achieve the EU’s climate and energy targets, the EU’s aim with the Taxonomy Regulation is to channel investments into sustainable projects and activities. In order to avoid greenwashing, the Taxonomy Regulation defines when an activity is “sustainable”. The Taxonomy Regulation is therefore the common classification system for sustainable economic activities.

According to the Taxonomy Regulation, only those economic activities that make a significant contribution to achieving environmental objectives are sustainable or “green”. At the same time, they must not significantly impair other environmental objectives.

Objectives of the EU Taxonomy Regulation

Evaluation standard

The following six environmental objectives represent the assessment standard:

Criteria

An activity is considered EU Taxonomy compliant (and therefore classified as sustainable) if it meets the following 4 criteria:

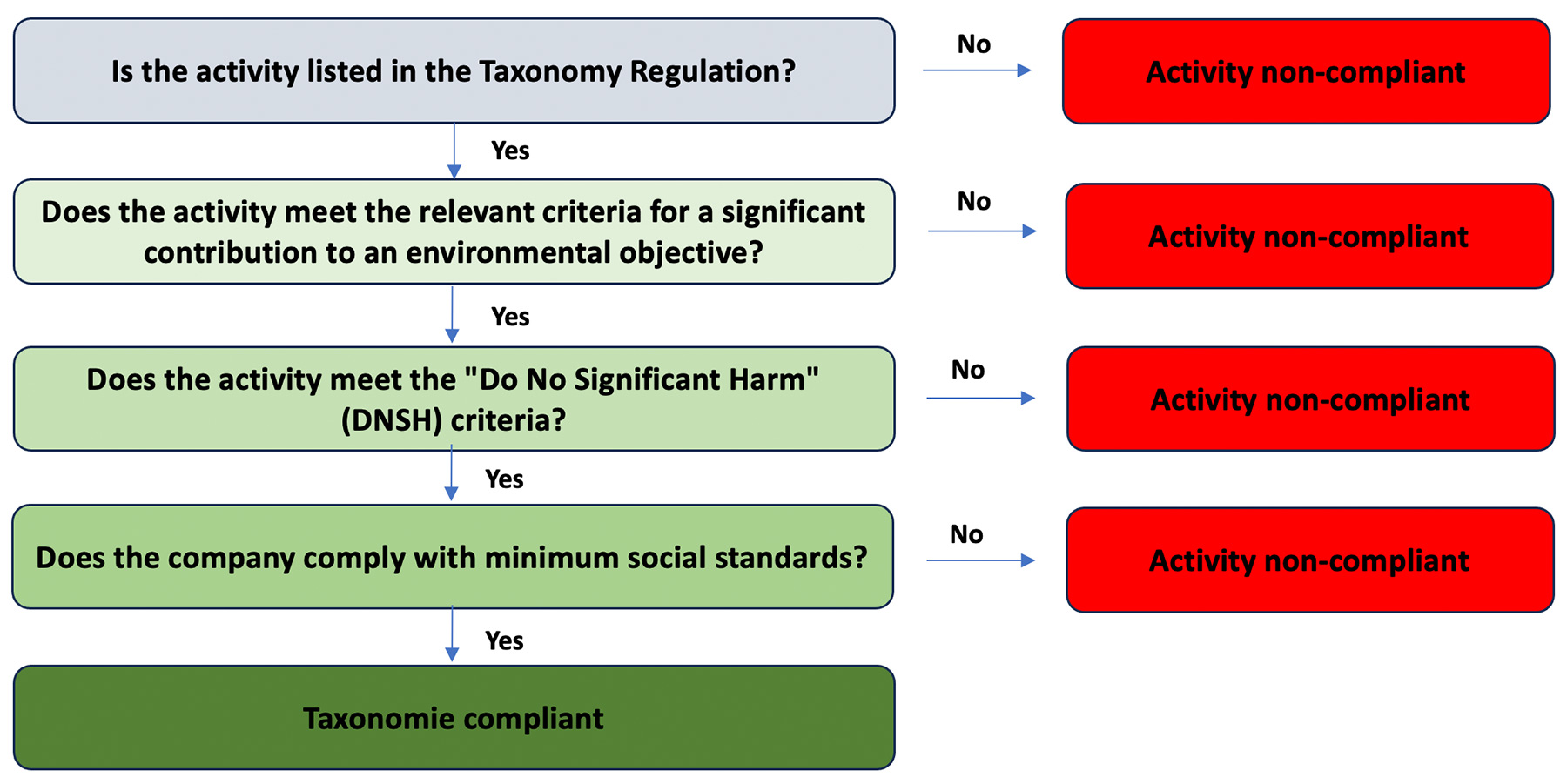

Procedure of the criteria check

Schematic process of the criteria check in accordance with the EU Taxonomy Regulation:

Delegated acts to the Taxonomy Regulation list the economic activities that contribute to an environmental objective. For this purpose, the technical assessment criteria are listed, compliance with which is not expected to have a negative impact on the other objectives. This means that if an activity is listed in a delegated act, it is taxonomy-compliant if it meets the technical assessment criteria and the minimum social standards.

Who is affected by the Taxonomy Regulation?

In principle, all companies that are required to publish a non-financial report as part of the management report in accordance with the CSRD (details can be found on the CSRD Reporting page) and financial market participants that invest in or advertise certain financial products are affected. For companies, this represents the link between the EU taxonomy and CSRD.

Company-related disclosure (Article 8 Taxonomy Regulation)

In order to improve non-financial reporting in practice and meet the increased demand for sustainability information, the European Commission published a revision of the Non-Financial Reporting Directive in December 2022 with the Corporate Sustainability Reporting Directive (CSRD) .

The CSRD extends the scope of non-financial reporting to all large companies as well as all small and medium-sized companies listed on the stock exchange. It also specifies the information to be reported. The proposal also authorizes auditors to audit the content of non-financial statements.

The European Commission has commissioned the European Financial Reporting and Auditing Group (EFRAG) to draw up European Sustainability Reporting Standards (ESRS). The ESRS specify which information must be reported by companies subject to the CSRD.

Non-financial companies must present the following in their management report:

Product-related disclosure (Articles 5, 6 and 7 of the Taxonomy Regulation)

Financial market participants must apply the taxonomy when designing their financial products. In the case of financial products that advertise environmental or social characteristics or that aim for sustainable investment, information on the investment methods and the use of the taxonomy for these products is mandatory.

This means that financial market participants are obliged to disclose information on how and to what extent the criteria for environmentally sustainable economic activities are applied when they offer financial products as environmentally sustainable investments or as investments with similar characteristics.

According to the Disclosure Regulation (EU) 2019/2088 (also known as the Disclosure Regulation or SFDR), financial market participants that invest in or advertise certain financial products must Disclose information on sustainability risks, the consideration of negative impacts and sustainable investment objectives.

The aim of the regulation is to better protect end investors through harmonized transparency regulations. Small investment advisory firms and insurance intermediaries with fewer than 3 employees are exempt.

The aim of the Disclosure Regulation is for all financial market participants to integrate ESG factors into their advisory process. This is intended to ensure that (institutional) investors incorporate ESG factors into their investment decisions.

For financial products that aim to achieve a sustainable investment, the following information must be disclosed in accordance with Art. 5 of the Taxonomy Regulation:

Financial companies are obliged to disclose additional information, for example:

“Financial market participants” pursuant to Art. 2 No. 1 of the Disclosure Regulation are as follows:

Articles 5 to 7 extend the Taxonomy Regulation to include taxonomy-related aspects. With reference to the SFDR, it distinguishes between three product categories (the content and type of presentation are specified by technical regulatory standards of the European Commission (Delegated Regulation (EU) 2022/1288)).

Support from risksafe ESG

We are happy to support you with our many years of experience in CO2 Management, the preparation and auditing of Sustainability Reports, Management Systems, Legal Compliance and as Environmental Verifiers in the

Our offer

Take advantage of our experience – you won’t find a higher level of expertise!

Our technical assessments have a high degree of recognition, particularly due to our state approval as an environmental expert and engineering office for environmental issues.