Obligation to prepare a CO₂ Balance Sheet

Based on the EU Corporate Sustainability Reporting Directive (CSRD) companies will have to disclose their greenhouse gas and CO2 emissions in future. Although this only affects companies with more than 250 employees and a turnover of more than 40 million, smaller companies will also have to deal with their CO2 emissions. To draw up a CO2 or greenhouse gas balance, all direct and indirect greenhouse gases (CO2, CH4, SF6, NF3, N2O, HFCs and PFCs) produced (sources) and removed (sinks) are determined or calculated within a spatial and temporal balance framework and recorded in a so-called CO2 balance.

All greenhouse gases are converted into CO2 equivalents according to their global warming potential (GWP).There are a number of synonyms for the term “CO2 balance”, including Greenhouse Gas Balance, Greenhouse Gas Balance, GHG Balance, Corporate Carbon Footprint (CCF), carbon footprint, process carbon footprint or corporate carbon footprint.

Standards for CO2 Balancing

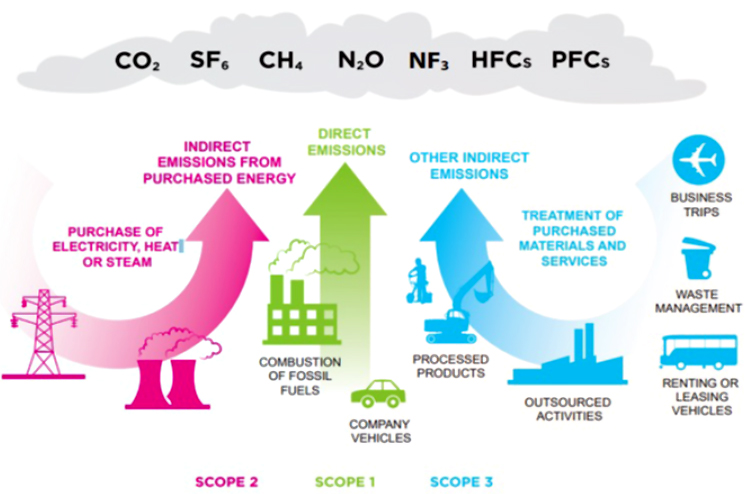

There are essentially two globally recognized sets of rules for corporate carbon accounting. These are the Corporate Standard of the GHG Protocol (“GHG Protocol”) and ISO 14064-1. Both standards regulate the framework conditions for carbon accounting and have similar requirements for a carbon footprint.In contrast to the GHG Protocol, ISO 14064-1 is “certifiable”, i.e. it also standardizes the review (“verification”) of the calculated greenhouse gas balance by an independent testing organization (certification). According to the GHG Protocol, greenhouse gas emissions are divided into the following 3 scopes:

ISO 14064-1

ISO 14064-1 divides greenhouse gas emissions into the following 5 categories:

Category 1: Direct GHG emissions

Category 2: Indirect GHG emissions from imported energy

Category 3: Indirect GHG emissions from transportation

Category 4: Indirect GHG emissions from products used by an organization

Category 5: Indirect GHG emissions associated with the use of the organization’s products

Category 6: Indirect GHG emissions from other sources

Right-hand image: Emission categories according to the Greenhouse Gas Protocol (EnergyAgency.NRW)

Procedure for the initial preparation of a carbon footprint

The following steps are usually taken to create a carbon footprint:

Benefits and advantages of a greenhouse gas or CO2 balance

Our offer

We are happy to support you in creating and updating your carbon footprint.

Our more than 20 years of experience with environmental management systems and the experience gained from a large number of prepared and/or verified carbon footprints enable us to recognize your requirements and needs precisely and to adapt the carbon footprint exactly to your requirements or not to apply excessive effort.

Our extensive experience with the verification of carbon footprints in the European Emissions Trading System (EU ETS) since 2005 guarantees you the highest level of expertise available on the market and thus a high level of credibility for your carbon footprint.

If the carbon footprint is to be verified externally, the requirements of the underlying standard(s) must also be taken into account. According to ISO 14064-1, these include the preparation of a greenhouse gas report, the assessment of uncertainties and the performance of internal audits.

Procedure for continuously updating the CO2 balance

Updating the carbon footprint, usually on an annual basis, is far less work than preparing it for the first time. It is important to take into account any changes in the framework conditions (e.g. new sources or sinks) and any necessary adjustments to the reference period in order to ensure a transparent comparison with the reference period.

External verification of the CO2 balance

To ensure the credibility of the carbon footprint, many companies have it checked, verified or certified by an external organization. Such verifications are carried out by major international certification organizations such as TÜV, LRQA, DNV or BV. In any case, an accredited testing organization for such verifications is recommended, as this significantly increases the credibility of the testing. Accreditation corresponds to a state license for the verification of greenhouse gas balances. LRQA, for example, currently has such an accreditation. We are happy to support you in the selection of the verification organization.